Exports to the EU are mainly fertilizers (ammonium nitrate, ammonia) and OXO alcohols.

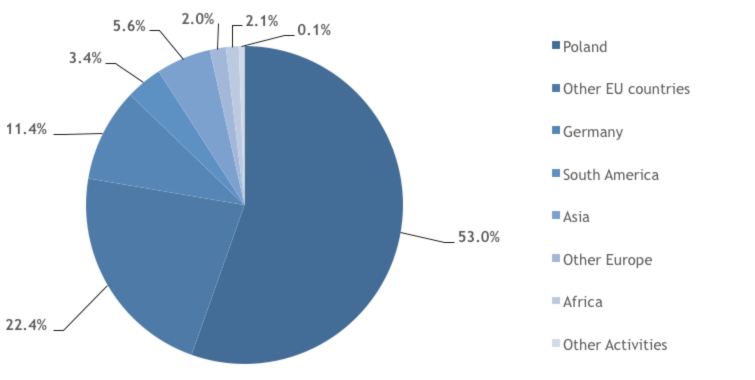

The Grupa Azoty Group enjoys a strong position in domestic and foreign chemical markets. Its products are mainly marketed to EU countries, particularly Germany, UK, the Czech Republic, Italy, France and Belgium.

Fertilizers and chemicals (urea and OXO alcohols) are the key products sold in the domestic market. Exports to the EU are mainly fertilizers (ammonium nitrate, ammonia) and OXO alcohols, whereas Asian exports are mostly caprolactam and polyamides, and South American exports include chiefly fertilizers.

Sales by geographies in 2014

Sources of strategic raw materials

The Group had one supplier whose share in the total cost of raw materials exceeded 10% − PGNiG S.A.

Natural gas

PGNiG S.A. supplied natural gas from the transmission network or from local sources under long-term agreements. Supplies from other trading partners were executed under short-term agreements. In 2014, the Grupa Azoty Group purchased 61.4% of its natural gas from PGNiG S.A. and the remaining 38.6% from other sources.

Phosphate rock

Phosphate rock was purchased under periodic or spot contracts, chiefly from North African producers, given the material’s abundance in the region, as well as the well-developed local sea logistics infrastructure. The Group is diversifying its procurement strategy, relying strongly on its own deposits in Senegal, which give it a vital competitive advantage. The situation in the phosphorite market is to a large extent driven by the situation in the fertilizers sector. The Grupa Azoty Group has in place a joint phosphate rock purchase programme for the production plants of Grupa Azoty POLICE and GZNF Fosfory Sp. z o.o.

Ammonia

The Group’s procurement strategy in this area is based on optimisation of intragroup ammonia supplies. The Grupa Azoty Group is Poland’s largest ammonia manufacturer, and operates several ammonia units. Apart from satisfying its own requirements, the Group sells surplus ammonia to external customers (chiefly Grupa Azoty POLICE and Grupa Azoty ZAK). Effective implementation of the procurement process largely depends on conditions prevailing on the fertilizer market and in the natural gas sector. The Group is the largest consumer of ammonia on the domestic market and in the region.

Propylene

The bulk of the Group’s purchases of propylene are made under annual contracts, with supplementary purchases made on the spot market. Propylene prices are driven to a large extent by oil prices.

In 2014, as in previous years, Western European markets were the main propylene suppliers.

Potassium chloride

Given the substantial natural resources and competitive commercial terms, producers from Russia and Belarus are the primary suppliers of potassium salt. Supplies are executed under quarterly contracts, with supplementary deliveries sourced periodically from Western Europe.

Phenol

The Group’s phenol procurement strategy is based on two primary sources – Western European and domestic suppliers. Also, the Company has secured regular supplies from Scandinavian producers to supplement the existing sources. The phenol market in 2014 was largely driven by benzene contract prices, which are the principal component of phenol pricing formulae. Furthermore, the Group has commenced work on developing its logistics infrastructure using the Group’s potential in this area.

Sulfur

The Grupa Azoty Group’s sulfur procurement strategy is based on optimisation of sulfur supplies from its own sources (Grupa Azoty SIARKOPOL) and supplies of petrochemical sulfur. This approach provides the Group with considerable flexibility in terms of the ability to secure supplies for the Group companies and to reduce purchase costs, and also guarantees the flexibility of supplies in the event of changes in demand for sulfur (Grupa Azoty SIARKOPOL is able to output more prilled sulfur by processing surplus molten sulfur). The Group is the largest consumer of liquid sulfur on the domestic market and in the region.

Methanol

Methanol is mainly supplied under one-year contracts, with supplementary purchases made on the spot market. Since Poland is not a methanol producer, the entire domestic demand is covered from imports. Thanks to the location of its Tarnów plant close to the Eastern border, the Group is able to maximise supplies from Russian sources, which are the cheapest in the region.

Benzene

Benzene is mainly supplied under one-year contracts, with supplementary purchases made on the spot market. Benzene is sourced chiefly from domestic and CEE suppliers. The Grupa Azoty Group is the largest benzene consumer in Poland. The Group has a joint procurement strategy, which gives it a significant competitive advantage. The benzene market is largely driven by the situation on the crude oil market and the global demand–supply balance, particularly in terms of benzene demand outside Europe.

Electricity

The Company and the Grupa Azoty Group companies purchased electricity from major Polish suppliers, i.e. PGE S.A., TAURON Polska Energia S.A. and ENEA S.A. Following a number of tenders for 2014, the Group companies executed electricity supply contracts as part of their existing framework agreements, and negotiated significantly reduced electricity prices, which were 10-15% lower than in 2013. It was possible to negotiate competitive contractual prices and terms thanks to the procurement strategy adopted by the Group, and in particular the procurement scale. Given the volatility of the electricity market and its changing legal framework, the Group’s policy was to purchase electricity under short-term contracts.